Leave data scientists and IT behind and jump in the driver’s seat with Aurora AI to automate analytics, forecasts, and predictions . . . Be hands-on in minutes

“Aurora AI demand forecasting, one year in advance, reduced forecast error 70%”

Omar Campbell, Vice President Demand Planning, International Vitamin Corporation

A LightZ™ model is built by its AI in minutes –

no programming nor IT support

LightZ™ cognitive AI gets you fast-to-value

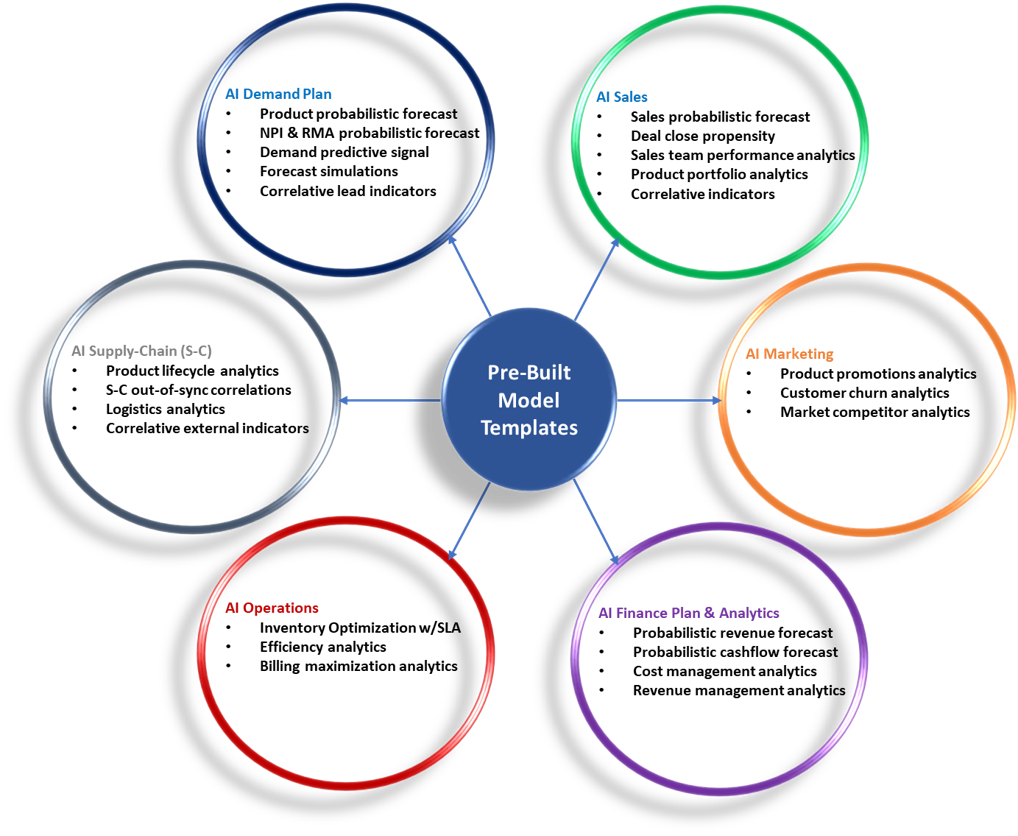

Load your data in LightZ™ and let its AI automatically deliver solutions for sales, finance, operations, and supply chain – zero coding

LightZ™ built-in comprehensive intelligent reporting/charting engine instantly delivers variance analysis, AI predictions, correlations, and statistics on all data

AI/statistical values are interpreted by an icon so you don’t have to be a statistician to know what the values mean

Lightz™ AI is Architected to be intuitive & practical

Supplement your ERP, CRM, Demand Plan, and EPM systems with deep AI analytics

LightZ library of built-in and interpreted math/statistics are automatically applied on data and rendered by a built-in reporting engine – zero coding

As such, LightZ™ powerfully delivers AI-Enabled analytics instantaneous through an intuitive user interface to put analytics in your hands and get immediate value

We are the experts. We have written the book on the topic of AI-enabled analytics.

Click the book or Amazon button to learn “How To” implement your digital transformation.

Our users come from

AI-Enabled Analytics Testimonials

Like artificial intelligence, this book promises a lot. And it delivers! By clearly explaining AI’s fundamentals and identifying the keys to its successful implementation, the book is essential reading for corporate executives, small business operators, and individuals running non-profit organizations.

John F Cogan

Senior Fellow, Stanford University Hoover Institution

Maisel, Zwerling, and Sorensen have created a brilliant primer for understanding and implementing AI programs. Rich with successful business case studies, their insights are essential to the success of any executive hoping to build a performance-based culture using data-driven decisions.

Steven S Myers

Serial Entrepreneur, CEO coach, author, and speaker

AI-enabled analytics is the next enabler of sustainable growth in today’s volatile, uncertain and hyper-competitive world. This guide lays out a practical approach to harnessing the power of data and analytics supported by relevant and insightful use cases. Whether deep into creating an analytics powerhouse or ready to embark upon the journey there are lessons that can help ensure implementation success and ongoing strategic value.